Sales activity in 2019 was slightly higher than forecasted, as stronger-than-expected price declines and easing mortgage rates helped support modest improvements for homes priced below $500,000. These improvements outweighed the losses for the higher-priced product.

As we move into 2020, we expect these trends in the market to continue – where improvements will be driven by the lower end of the market and challenges will persist in the higher end. Despite challenges in the higher end of the market, overall sales activity is expected to improve by two per cent.

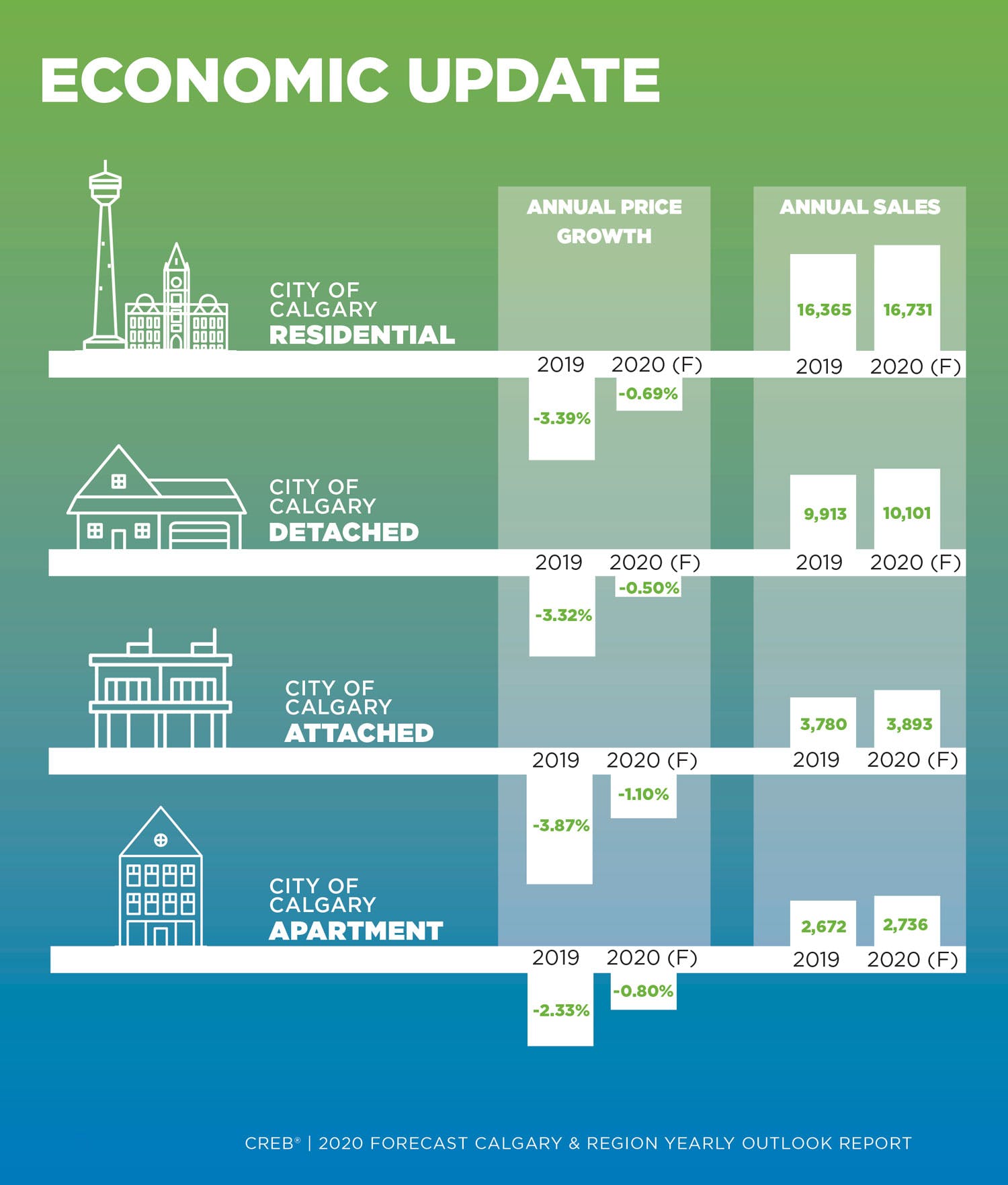

Improving sales and easing inventories are expected to help reduce the oversupply. These reductions will help shift the market closer to balanced conditions, but the pace of adjustment is expected to be slow. The reductions in oversupply are expected to slow the pace of price declines, as prices are forecasted to ease by less than one per cent. Like 2019, divergent trends are expected to remain the theme of 2020. Relatively affordable product is expected to record some improvements, while persistent oversupply will weigh on the higher end of the market.

While the housing market is generally expected to move to more stable conditions, there is some downside risk to the forecast this year.

Much of this risk is coming from employment expectations. Full-time job growth did improve in 2019, but at the end of 2019, Calgary and many other areas of the province recorded job losses. Some growth is expected in 2020, but recent job losses could spill into the early part of 2020, impacting confidence, housing sales and prices in 2020.

Detached Housing Market

2020 MARKET FORECAST:

The detached market has struggled more than other sectors following the stress-test change occurring in 2018. However, after several years of adjustments, and steeper price declines in 2019, we are expecting to see some signs of improvement in 2020. Further declines in inventory, coupled with expected sales growth, will help reduce the oversupply in the market and slow the pace of decline in prices.

However, as was the case in 2019, the market will continue to see divergent trends based on price range. Price declines, favorable lending rates, lower wages, and job growth that is occurring in non-traditional and lower-paid sectors are creating conditions that support modest demand growth for lower- priced product. In addition, we benefit from a younger buyer demographic that is looking for homeownership options. These trends should support improvements in the lower price ranges, both in terms of sales growth and price improvements.

While improving conditions in the lower end can eventually spill into the upper end of the market, this is not expected to occur over the next year. The lack of employment growth in higher-paid sectors and the risk associated with economic prospects will continue to weigh on demand for higher-priced homes. The elevated supply-demand balances in those ranges will likely continue to impact prices until they ease enough to support changes in supply and demand.

Attached Housing Market

A LOOK BACK AT 2019 (TOWNHOME SECTOR):

-

The relative affordability of this product type, coupled with price adjustments in this segment, supported sales growth in the resale market. While sales improved across most districts, the largest gains occurred in the South East district.

-

New listings continued to decline across most districts, supporting reductions in inventory levels. The one exception is the City Centre district, where, despite improving sales, the rise in new listings was enough to prevent any reductions in overall inventory levels.

-

The balance between supply and demand improved, mostly for product priced below $400,000. Citywide, this helped prevent further price slides in the second and third quarters, slowing the annual decline in prices. However, overall, row prices remained four per cent lower than last year’s levels and 13 per cent lower than 2015 annual highs.

Apartment Housing Market

2020 MARKET FORECAST:

The apartment sector is typically the most affordable sector in the market. However, it did not receive the same boost in sales that the attached sector saw, likely due to competition coming from the new-home market. Competition from the new-home market and excess supply in the resale market have caused prices to decline for four consecutive years.

In 2020, easing prices and tighter rental-market conditions are expected to support modest sales growth in this sector. However, growth will be limited, as persistent competition from the new-home sector will continue to impact resale demand. At the same time, supply levels should continue to slowly ease, but this is not expected to be enough to support balanced conditions. Persistent oversupply is expected to continue to weigh on prices, but the pace of decline should ease, with an annual forecasted decline of nearly one per cent.